Positive Momentum Meets Economic Crosswinds

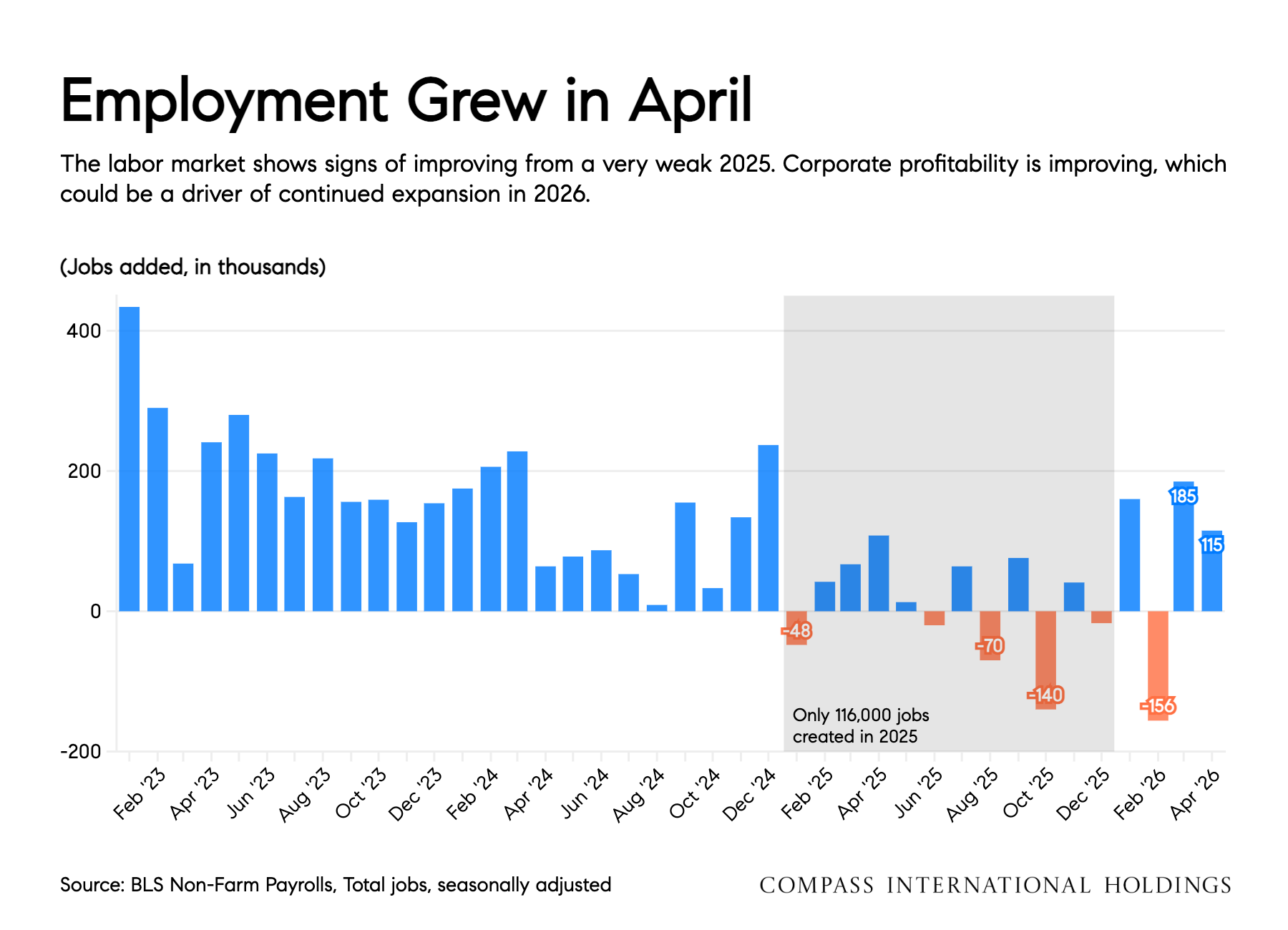

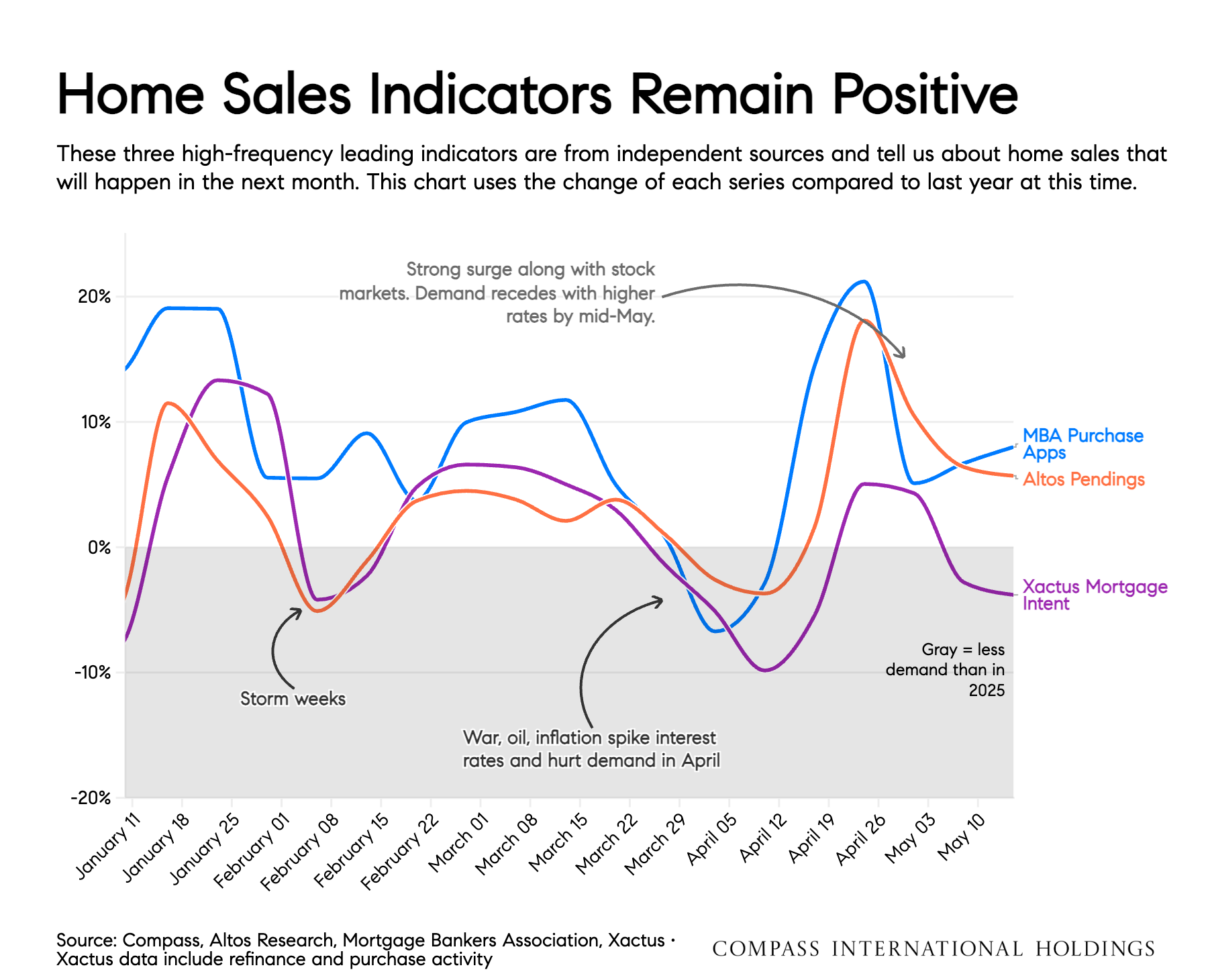

As we roll into peak homebuying season at the end of May, the housing market has (finally) turned in some positive momentum and the economy is showing some positive reversals of recent trends. Equities markets have surged to new highs. The long-sluggish labor market has shown some green shoots of improvement. Unemployment and initial jobless claims remain relatively low and, in the latest data, hiring and job creation seem to have improved.

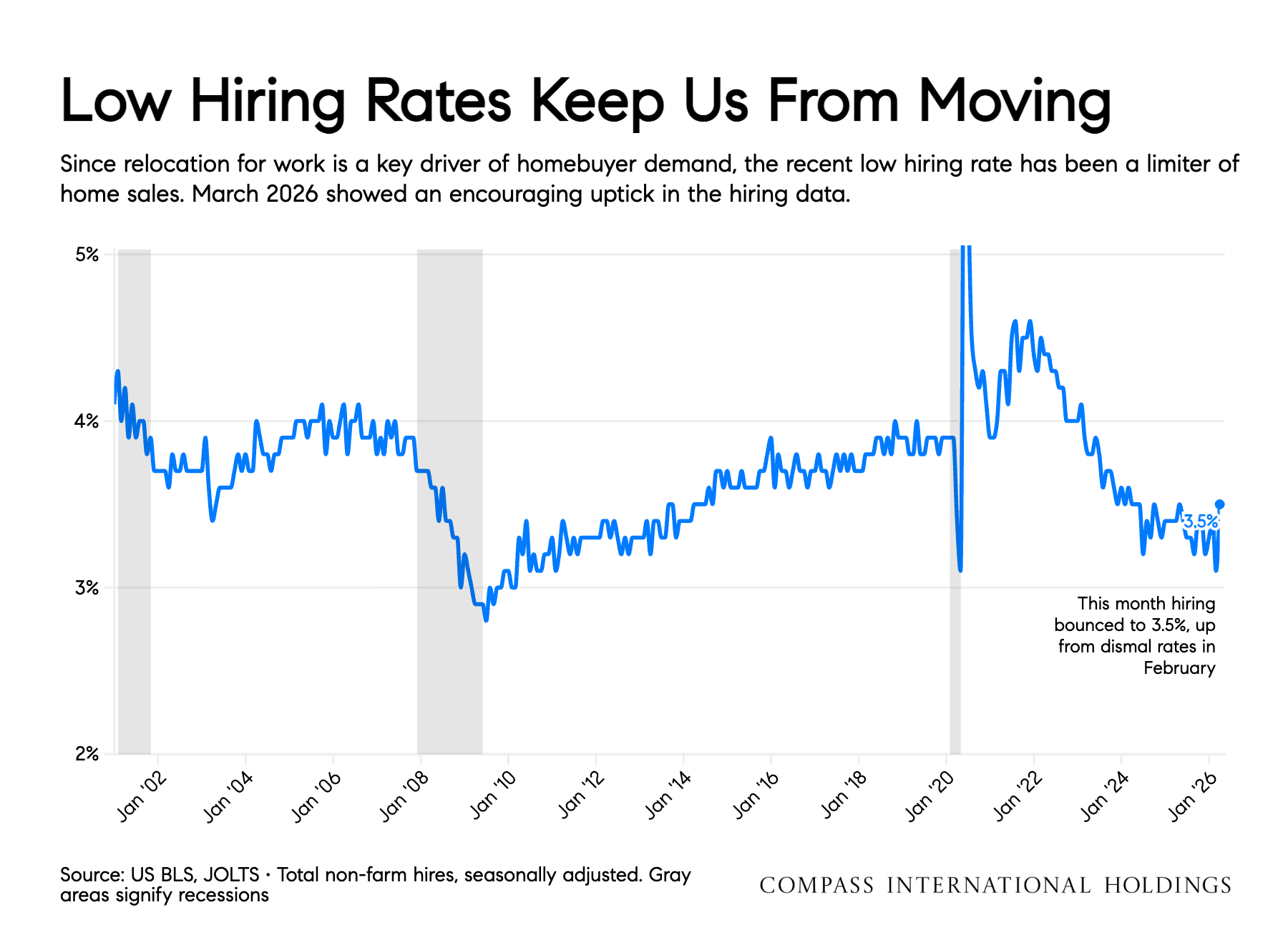

In this year’s housing cycle, we’re focused more on the hiring rate in the economy rather than the usual unemployment numbers. Since relocation-for-work is one of the big drivers of housing demand, a very low hiring rate in 2026 continues to be the biggest drag on housing demand, after affordability. If companies are not hiring quickly, there are fewer people moving for work.

In March, the hiring rate data was as low now as the bottom or the pandemic shutdown. But in April the data rebounded to 3.5%. Continued growth in hiring will be important if home sales are going to grow meaningfully for the rest of 2026.

The negative news in this spring’s economy is around inflation. Energy costs, tariffs, and government spending are all contributing to rising prices. The war-driven uncertainty has driven energy prices sharply higher and the inflation impacts are only just hitting the economy now.

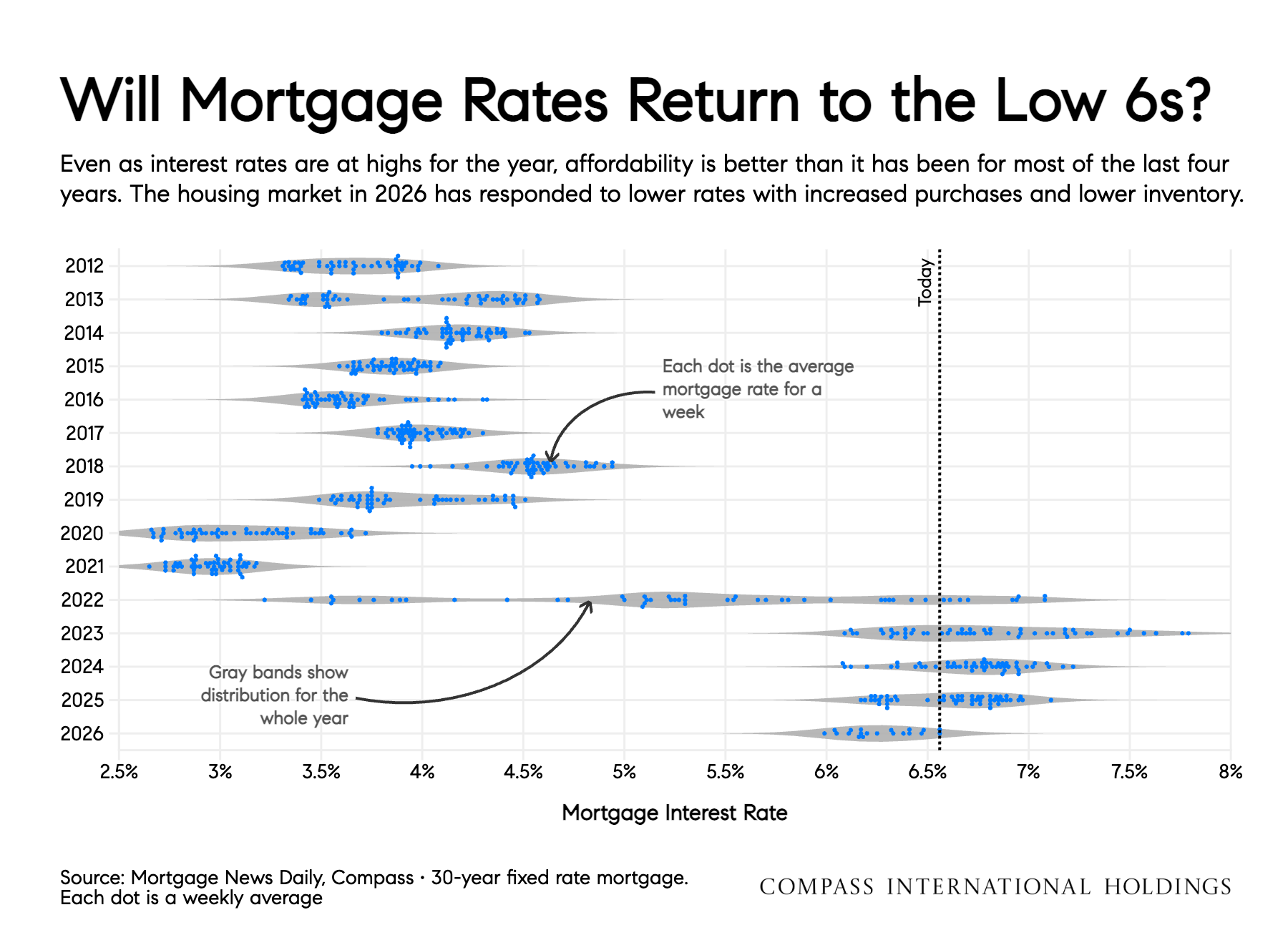

Unfortunately, higher inflation and stronger employment is not the economic setup that tends to push interest rates lower. As of mid-May, mortgage rates responding to inflation news are at their highest levels of the year. Don’t look to the Fed for interest rate relief until the inflation trend turns.

An interesting question is whether a booming stock market is enough to move the needle on the housing market. We can see the AI boom directly in San Francisco home prices and rents, but it remains to be seen whether middle America feels a wealth boom from equities or a cash crunch from inflation, and how that impacts home buying activity through the summer.

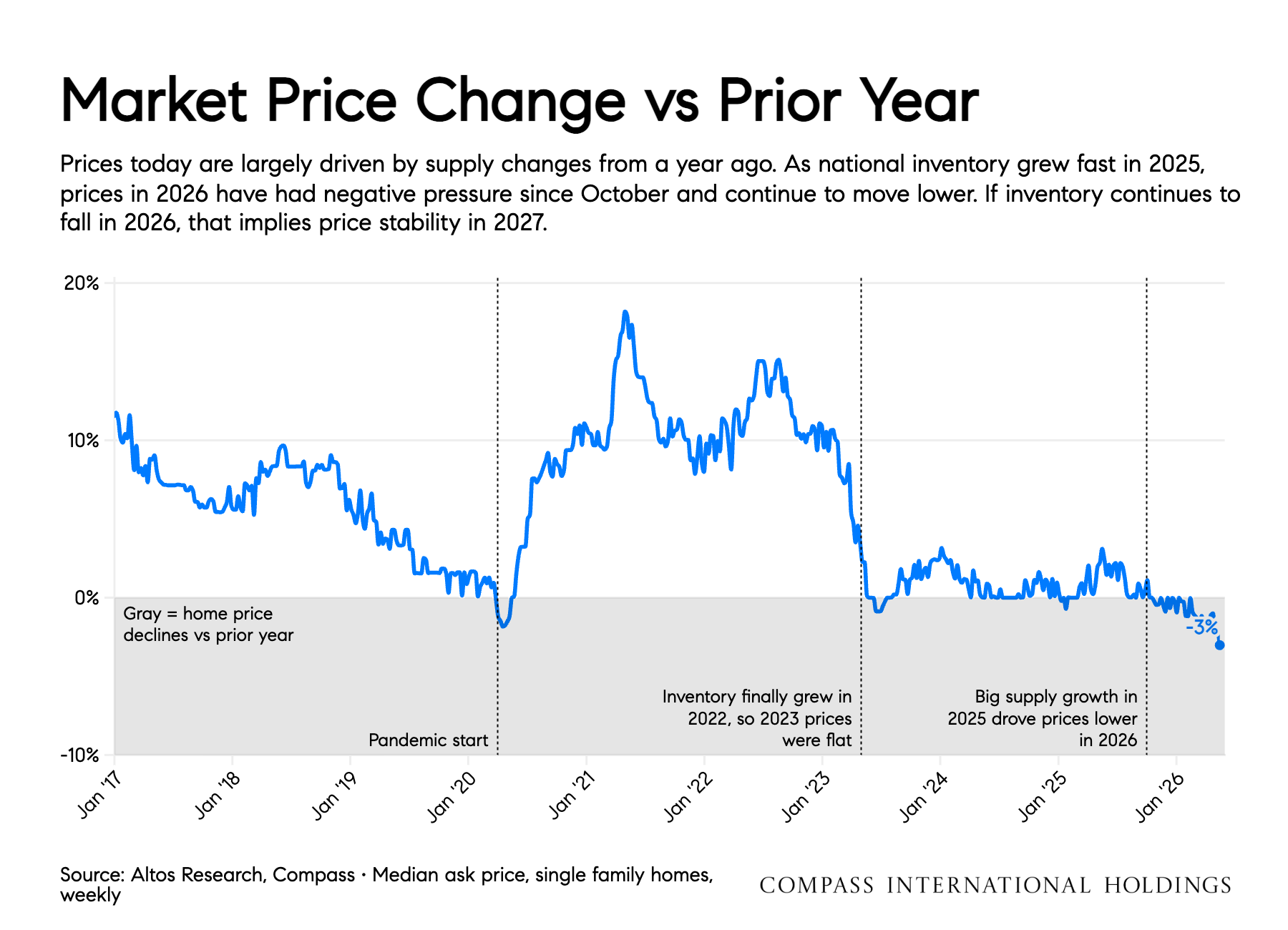

As mortgage rates gradually declined over the last year, the inventory story has changed too. After growing quickly for several years, the supply of homes on the market is now unchanged from last year and could be heading lower. Shrinking inventory would be a big surprise for most market watchers in 2026.

Because supply has been growing nationally for years, we can now measure the negative price pressures in much of the country. If inventory continues to decline in 2026, that implies price stability in 2027.

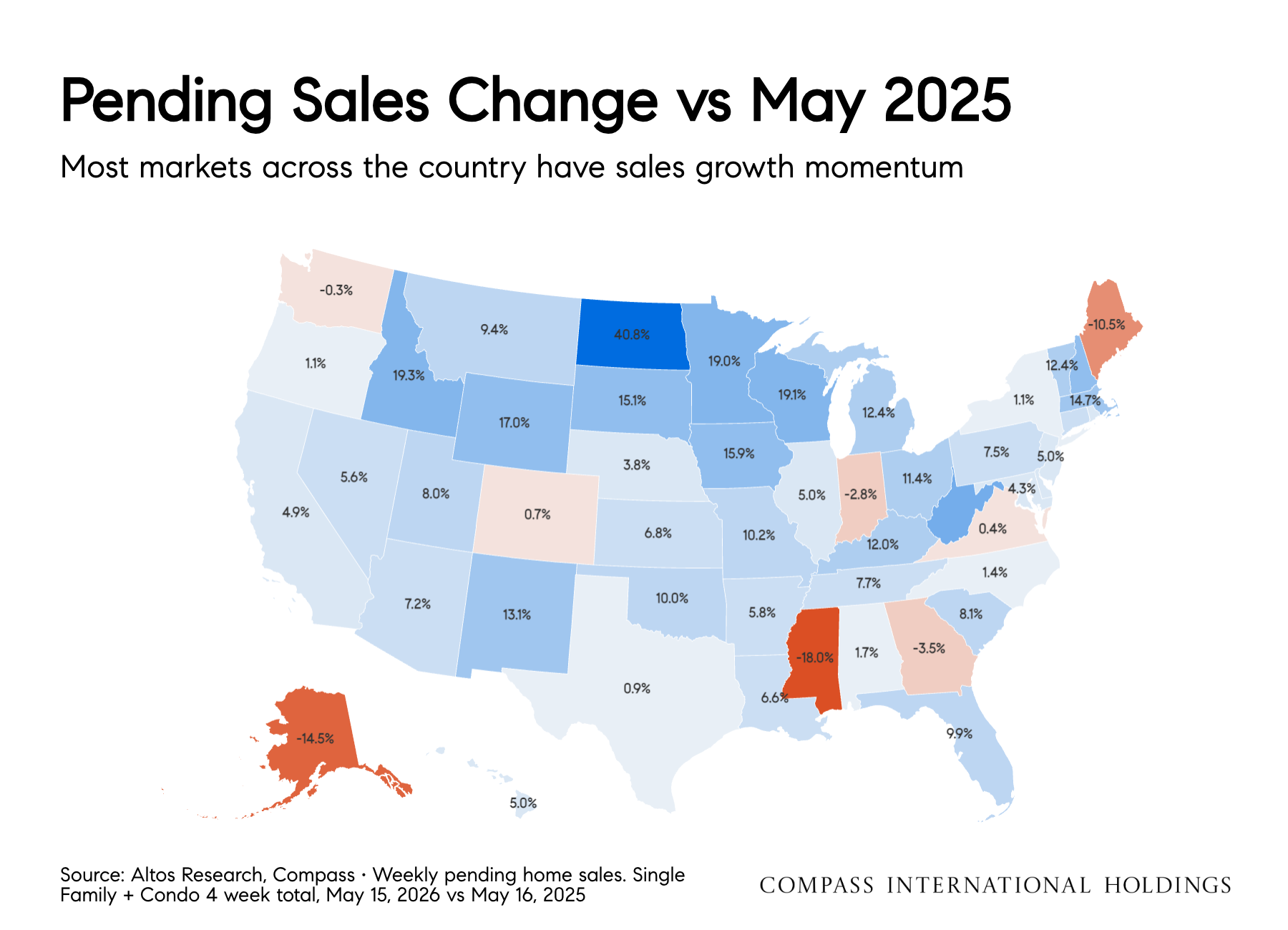

I was in Austin recently for a Compass event. That city’s market may be on the cusp of a turnaround, finally. After four relentless years with inventory climbing, the supply of homes on the market in Austin (Dallas too) is now below last year and ticking downward. Anyone in the Austin market knows that there have been home price pressures for several years, is this finally the inflection point? Stay tuned.

Mike Simonsen

Chief Economist | Compass International Holdings